The following sections explain how management can assess potential causes for a favorable or adverse material price variance and devise a suitable response to the variation. If a budget variance is unfavorable but considered controllable, then perhaps there is something management can do immediately to rectify the problem. If the budget item is not something management directly controls, then perhaps they need help crafting a new business strategy in order to survive and grow. Knowledge of this variance may prompt a company’s management team to increase product prices, use substitute materials, or find other offsetting sources of cost reduction.

What is the formula for the direct materials price variance?

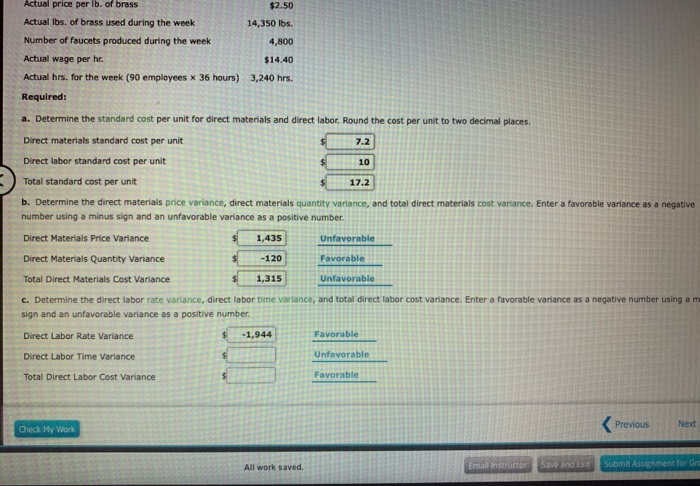

The standard quantity is the expected amount of materials used at the actual production output. If there is no difference between the actual quantity used and the standard quantity, the outcome will be zero, and no variance exists. If the actual price paid per unit of material is lower than the standard price per unit, the variance will be a favorable variance. A favorable outcome means you spent less on the purchase of materials than you anticipated. If, however, the actual price paid per unit of material is greater than the standard price per unit, the variance will be unfavorable. An unfavorable outcome means you spent more on the purchase of materials than you anticipated.

Create a Free Account and Ask Any Financial Question

- The standard cost is typically derived from historical data, industry benchmarks, or predetermined budgets, while the actual cost is recorded during the production process.

- Analyzing direct material variance is a powerful tool for businesses aiming to maintain cost control and enhance profitability.

- If more than 600 tablespoons of butter were used, management would investigate to determine why.

- This cross-functional collaboration ensures that all aspects of the business are aligned towards achieving cost efficiency.

- Specifically, knowing the amount and direction of the difference for each can help them take targeted measures forimprovement.

Finance Strategists is a leading financial education organization that connects people with financial professionals, priding itself on providing accurate and reliable financial information to millions of readers each year. The articles and research support materials available on this site are educational and are not intended to be investment or tax advice. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Finance Strategists has an advertising relationship with some of the companies included on this website.

Direct Materials Quantity Variance: Definition

A financial professional will offer guidance based on the information provided and offer a no-obligation call to better understand your situation. Someone on our team will connect you with a financial professional in our network holding the correct designation and expertise. Ask a question about your financial situation providing as much detail as possible. Our mission is to empower readers with the most factual and reliable financial information possible to help them make informed decisions for their individual needs. Our writing and editorial staff are a team of experts holding advanced financial designations and have written for most major financial media publications. Our work has been directly cited by organizations including Entrepreneur, Business Insider, Investopedia, Forbes, CNBC, and many others.

Understanding direct material variance is crucial for businesses aiming to maintain cost efficiency and improve profitability. This concept involves examining the differences between expected and actual costs of materials used in production, providing insights into potential areas for financial improvement. A favorable materials quantity variance indicates savings in the use of direct materials. An unfavorable variance, on the other hand, indicates that the amount of materials used exceeds the standard requirement. Direct materials price variance account is a contra account that is debited to record the difference between the standard price and actual price of purchase. For Boulevard Blanks, let’s assume that the standard cost of lumber is set at $6 per board foot and the standard quantity for each blank is four board feet.

Fundamentals of Direct Materials Variances

Additionally, regular audits of the production process can identify areas for improvement and help maintain optimal material usage. The material price variance in this example is favorable because the company was able to get the materials at a lower cost compared to the budget. The direct material price variance is also known as direct material rate variance and direct material spending variance. Our purchasing department was able to find materials for less than our standard, saving us a significant amount of money, which in turn improves the bottom line, which means this is a favorable variance.

An unfavorable outcome means you used more materials than anticipated to make the actual number of production units. If a company’s actual quantity used exceeds the standard allowed, then the direct materials quantity variance will be unfavorable. instant form 1099 generator This means that the company has utilized more materials than expected and may have paid extra in materials cost. With either of these formulas, the actual quantity used refers to the actual amount of materials used at the actual production output.

In a movie theater, management uses standards to determine if the proper amount of butter is being used on the popcorn. They train the employees to put two tablespoons of butter on each bag of popcorn, so total butter usage is based on the number of bags of popcorn sold. Therefore, if the theater sells 300 bags of popcorn with two tablespoons of butter on each, the total amount of butter that should be used is 600 tablespoons. Management can then compare the predicted use of 600 tablespoons of butter to the actual amount used. If the actual usage of butter was less than 600, customers may not be happy, because they may feel that they did not get enough butter.